Covenant misses expectations in noisy Q4

Covenant Logistics Group highlighted several achievements during 2022, including generating more than $1 billion in freight revenue and achieving an all-time high for full-year earnings per share, in its fourth-quarter report released Wednesday after the market closed. However, it also sees the current overhang on freight markets lingering for a while.

“Despite these unprecedented achievements, our fourth quarter results undoubtedly reflect sequential softening in the freight market, continued inflationary pressure and the cost of significant excess equipment,” David Parker, chairman and CEO, stated in a news release. “While we anticipate improved equipment related costs in 2023, we believe the freight market, as a combination of freight rates and volumes, will remain unfavorable compared to the prior year for the next several quarters.”

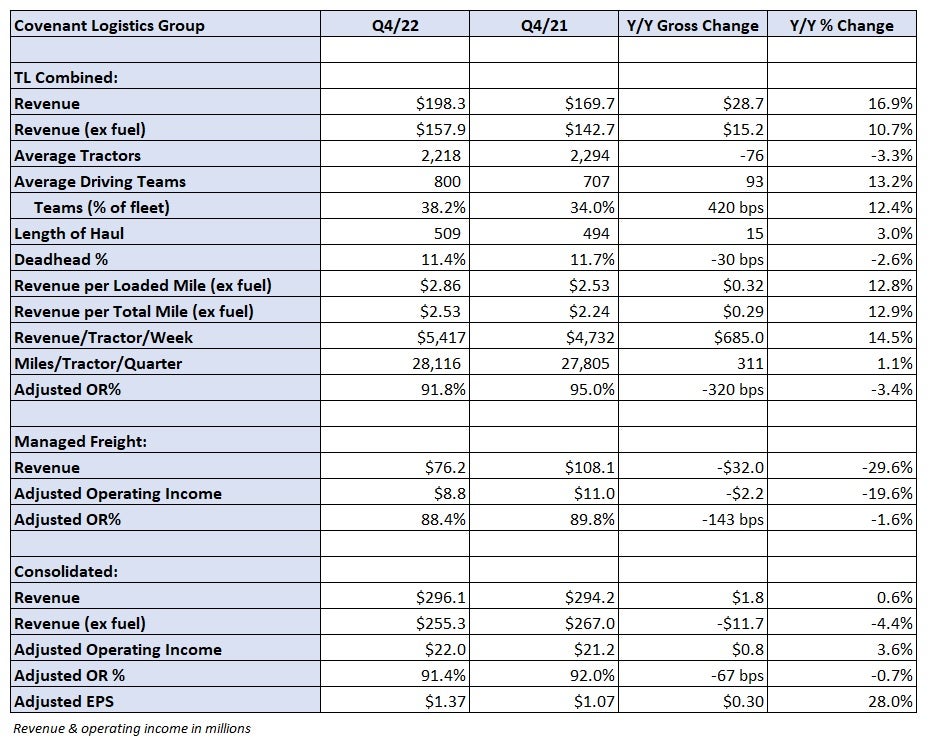

Covenant (NASDAQ: CVLG) reported adjusted earnings per share of $1.37 in the quarter, 5 cents shy of the consensus estimate, according to Seeking Alpha. Full-year EPS of $5.84 came in below management’s expectation of “approximately $6” and the fourth-quarter result was light of implied guidance of $1.54.

A fourth-quarter headline EPS number of 81 cents excluded 57 cents per share in incremental expenses tied to onboarding several new trucks during the period in efforts to “aggressively reduce the average age of our equipment.” The actions are expected to reduce maintenance expenses and improve fuel economy and driver satisfaction over time.

Broken down, the nonrecurring items included 43 cents ($7.5 million) in costs associated with breaking leases and the disposal of equipment. A hit of 14 cents per share ($2.5 million) reflected costs associated with carrying excess and underutilized equipment during the transition period. The average tractor age was lowered to 2.1 years during the quarter, flat year over year (y/y) but down from 2.4 years during the third quarter.

“The early lease abandonment and disposal charge relates to tractors pulled from operations during the fourth quarter, which have been the source of significant operational headwinds throughout the year due to poor fuel economy, unusually high maintenance costs and elevated down time,” the news release stated. “Because we have no intended future use for these units, we have abandoned the right of use asset associated with the leases, which extend through the fourth quarter of 2023.”

The adjusted EPS number also benefited from an 8-cent tailwind in higher gains on equipment sales and a lower tax rate when compared to the year-ago period.

Covenant’s ownership interest in Transport Enterprise Leasing, an equipment leasing company, contributed 21 cents per share during the quarter, which was 2 cents lower y/y.

Q4 takeaways

Revenue in Covenant’s truckload segment increased 17% y/y to $198 million, 11% higher excluding the impact from fuel surcharge revenue. Freight revenue per tractor per week increased 15% to $5,417 on an average fleet count that was 3% lower as the company exited unprofitable dedicated accounts. The dedicated fleet was down 10% y/y to 1,318 units.

The expedited fleet recorded a 17% y/y increase in freight revenue per truck per week compared to the dedicated unit, which logged a 6% increase. The jump in expedited revenue per unit was the result of hauling Hurricane Ian relief freight for the Federal Emergency Management Agency in October.

The adjusted operating ratio for the combined TL fleet was 91.8%, 320 basis points better y/y. The expedited unit recorded an 88.6% adjusted OR (360 bps better y/y) while the dedicated segment reported a 96.2% adjusted OR (160 bps better). Cost headwinds included a compensation line that was 310 bps higher y/y as a percentage of revenue. Seventy percent of that increase was tied to higher driver pay and benefits expenses. Insurance claims expense was up 150 bps y/y.

Revenue in the managed freight segment fell 30% y/y to $76 million. A tough comparison to the prior year and fewer loads from Covenant’s TL units were the culprits. Adjusted operating income was down 20% but the segment’s OR improved 140 bps to 88.4%.

“Revenue and operating income in this segment are expected to fluctuate with changes in the freight market and our percentage of contracted versus non-contracted freight,” said Paul Bunn, president and chief operating officer.

The company did not disclose changes in its managed freight contract-spot mix for the quarter.

Covenant’s guidance calls for net capital expenditures between $75 million and $85 million in 2023, which includes $87 million to $97 million in equipment purchases. On Jan. 13 it sold a terminal in Tennessee, which netted $12 million that will offset capex spending during the year in addition to other equipment sales.

Covenant recorded $48 million in net capex during 2022.

“As we look toward 2023, we anticipate a very difficult freight environment for at least the first half of the year which could compress rates and margins when compared to 2022,” Parker concluded. “However, we believe our more resilient operating model, together with the steps we are taking to reduce costs and inefficiencies, will mitigate a portion of our historical volatility throughout economic and freight market cycles.”

Covenant will hold a conference call to discuss results with analysts on Thursday at 10 a.m.